What happened to Early Access graduates in 2026 so far?

Also: Steam's tag changes and lots of news.

[The GameDiscoverCo game discovery newsletter is written by ‘how people find your game’ expert & company founder Simon Carless, and is a regular look at how people discover and buy video games in the 2020s.]

We’re back, and thanks for holding down the fort by ‘doing things on the weekend’ and ‘actually relaxing’, before GameDiscoverCo shoves another few thousand words of PC/console game discovery analysis in your general direction. (We appreciate you.)

Before we start, apologies, but we’re not following XBOX’s lead & rebranding to GAMEDISCOVERCO. We do think Xbox’s new management should fess up to their true all-caps inspiration, though - Princess Donut from the Dungeon Crawler Carl series. (“I AM YELLING, XBOX”.)

[THE DEEPEST PC/CONSOLE DATA? You can get a free demo of our GameDiscoverCo Pro company-wide ‘Steam deep dive’ & console data by reaching out today - >90 orgs have it. Or, signing up to GDCo Plus gets the rest of this newsletter and Discord access, plus more.]

Game discovery news: shortform hits are trending

Let’s start things out by a look at game discovery & platform news, which goes a bit like this:

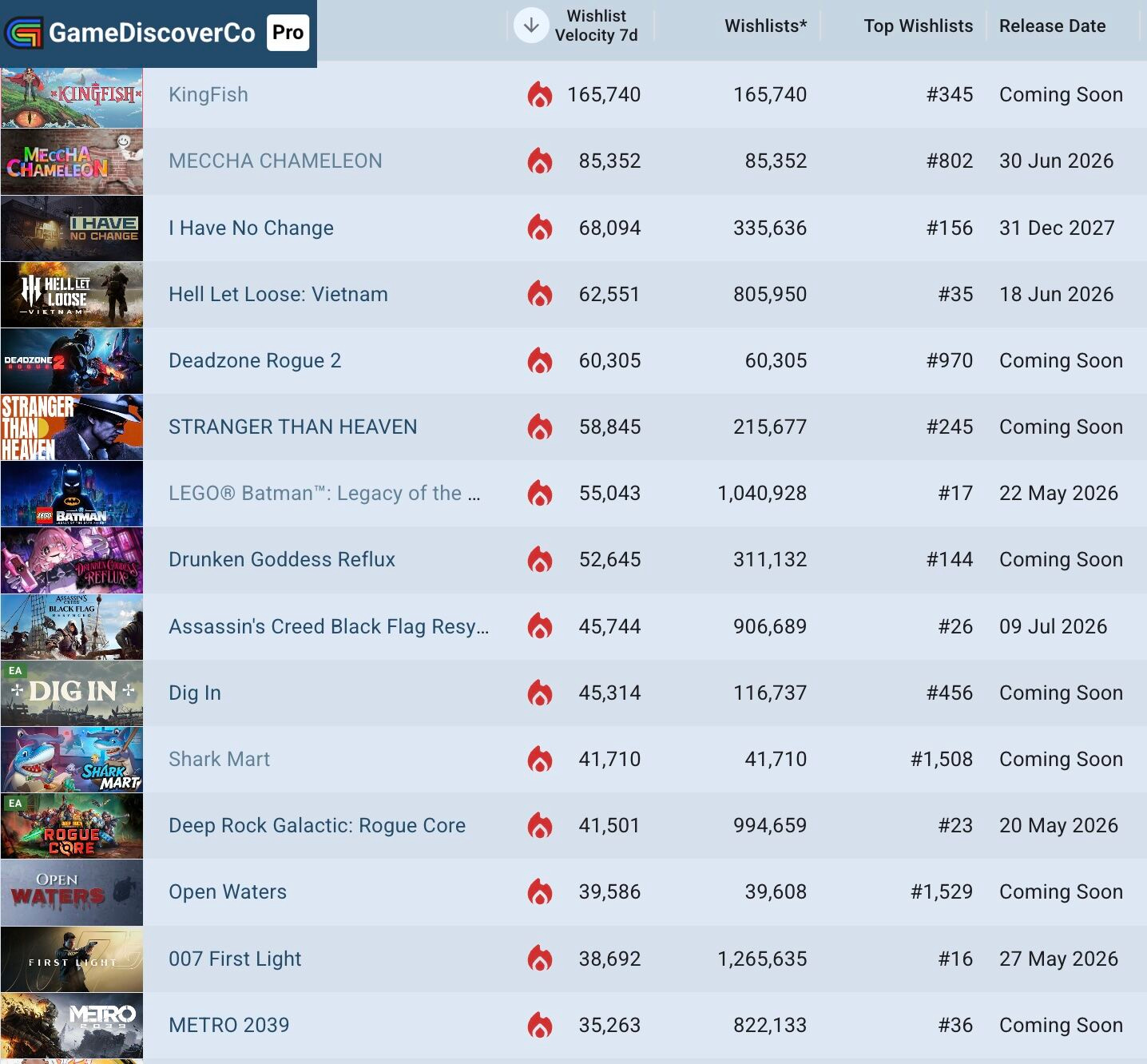

Looking at top GDCo Pro ‘trending’ games by 7-day wishlists (above), Paid/organic shortform video promos' based on viral concepts are hot, as shown by 2-player asymmetric co-op title KingFish (#1), which builds on a Wandering Village vibe, and Meccha Chameleon (#2), a 'paint your player' Prop Hunt-style concept.

Other new entries include roguelite FPS sequel Deadzone Rogue 2 (#5) and co-op 'sharks disguised as dolphins' friendslop Shark Mart (#11). Elsewhere, Hell Let Loose: Vietnam (#4) tops 800k WLs as it reveals a release date, and the Yakuza-y Stranger Than Heaven (#6), and Lego Batman (#7) are also cruising along nicely.

As rumored, PlayStation is turning a dial that says ‘exclusivity’ on it and constantly looking back at the audience, per Bloomberg’s Jason Schreier: “PlayStation studio business CEO Hermen Hulst told staff in a town hall Monday morning that the company's narrative single-player games will now be PlayStation exclusive.”

A sobering post from small dev studio CEO Jake Simpson: “Everyone keeps saying ‘Oh, if we can survive this year, pubs will need product; they'll open their purses when that happens’, and we've been saying that for 2-3 years.. and it's Not. Happened… try getting a budget of $3-4m out of anyone right now, see what happens.” (It largely true.)

Looks like “a bill focused on maintaining long-term playable access to online games has passed out of the California Assembly’s appropriations committee, setting up a floor vote by the full legislative body.” But it needs to pass Assembly, Senate and gov signature. (BTW: the ‘chilling effect’ on server-based games of any size prob. needs debating..)

GamesBeat has some interesting creator interviews on Epic’s UEFN payout changes, with January’s addition of monetizing based on in-island item purchases helping to “generate meaningful revenue from smaller experiences that wouldn’t have been profitable under Fortnite’s pre-existing engagement payout system.”

Game consoles? Pricy and getting pricier, points out this GameSpot editorial, saying: “Consoles are becoming too expensive for all but the most dedicated gamers to justify - especially when gamers in their teens and early 20s have grown up in a world where a console is no longer needed to play the vast majority of games.”

An interesting PlayStation 5 OS experiment: “a new Welcome Hub widget that’s currently in Beta… reveals the top ten games in your country, with total player numbers for the week”, and also has a ‘trending games’ option showing surging popularity (by %). Top 3 WAU listed at one point were: “Fortnite: 14.6m, GTA 5: 5.13m, Minecraft: 4.97m.” (We think that’s worldwide WAU - we’ll see if they keep this feature.)

Today in mobile game UA insanity (efficiency?): even Royal Kingdom is running unrelated (some say ‘fake’) paid ads to get people to initially play it: “Welcome to 2026, where the top-grossing match-3 in the world won’t even show you a match-3 in its top creative.”

Here’s a useful post on how to network/pitch games at video game events, explaining the formats (B2B matchmaking, pitching sessions, indie showcases mixers). Veterans may be fine, but for the newer folks, tips like ‘build buffer time into your schedule’ and ‘have a system for what happens after each meeting’ are handy.

How popular are Steam third-party events nowadays? Very. Celine Tricart explains what happened when 1,371 games (!) applied to her ‘Out Of The Box Games’ showcase, noting: “At that scale, deep curation becomes almost impossible.” (Worth thinking about when Valve showcase applications go weird, maybe…)

OUR SPONSOR: Trapster — Creator Game Marketing Platform

Trapster is a new way to grow your Steam wishlists. You launch a campaign, gaming creators make short-form videos on TikTok, YouTube Shorts and Reels, and you pay only for real views. Everything is built around driving wishlists.

No flat fees, no paying for content that flops. Your budget goes directly toward actual reach and wishlist growth. CPM-based model means you only pay when people actually watch, and every view is a potential wishlist.

GameDiscovery readers get 50% off platform fees on your first $5K. Sign up at Trapster.gg

Early Access graduates in 2026: what happened?

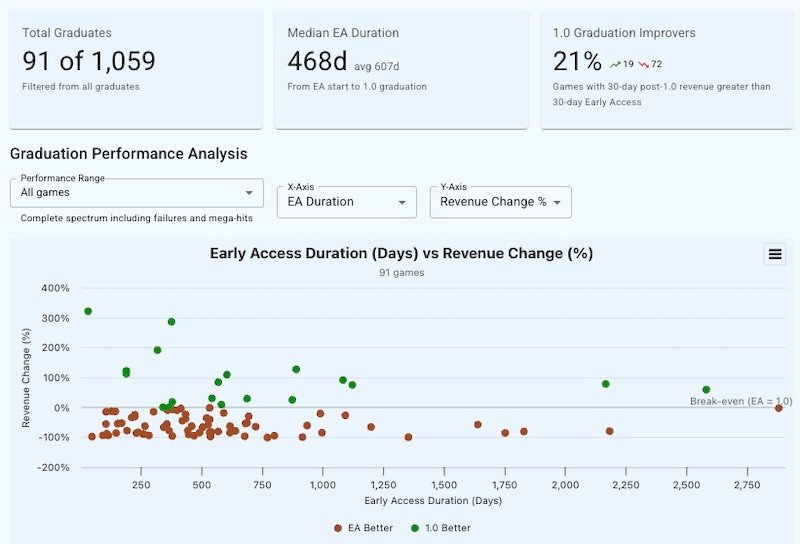

Sometimes we build tools for GameDiscoverCo Pro and then move on. Mistake! We took a look at our new Steam Early Access ‘graduates’ data back in late 2025. But now we’re partway through 2026, we thought we’d check back in to see if any trends had changes, and highlight particular high and low (revenue and conversion) performers.

Above is the chart we auto-generate for games 1.0 released in 2026 so far, specifically gated to “Paid games with >5,000 copies sold or free games with >$10,000 revenue in first 30 days of Early Access”, so we don’t get insane outliers. And the takeaways are clear.

Specifically, 2026’s Steam Early Access Graduates thus far have similar stats to 2025: of the 91 games we tracked, they were in Early Access for a median of 1 years and 3 months (one month longer than in 2025), and only 21% did better at 1.0, revenue-wise, than at Early Access launch. (This compares to 20% in 2025 - very similar.)

But what’s really interesting is when you look at the titles with the biggest 1.0 release by raw revenue so far in 2026. Our estimates compare incremental 1.0 revenue (30 days post-launch) to their first 30 days $ in Early Access. We also included their total LTD Steam revenue, cos that’s important context:

Obviously, these numbers aren’t perfect (we trend somewhat low on revenue for some ‘core’ genres like strategy), but they give a good idea of games doing well at 1.0 so far this year. Some comments on them:

There’s a lot of strategic games in the mix, which makes sense feature-wise: given that the best way to do Early Access is to build a ‘finished’ game but layer new features on top of it, seeing expandable games like Timberborn, Shapez 2 and Terra Invicta high up the charts makes sense.

Outperformers at 1.0 are often good games that get recognized late: for titles like clever roguelite Sol Cesto and the deep, complex The Last Starship, it’s almost disappointing there wasn’t more interest earlier. (There’s exceptions, like the Project Zomboid-ish HumanitZ, which has motored on nicely the whole time.)

These games represent a ‘hidden’ class of later success: when a game spikes up at 1.0, it’s not always that obvious or checkable. That’s why we like this view. Not all of these titles are profitable - for example, ARPG Dragonkin: The Banished surely cost Nacon a lot more than it’s made, even multiplatform. But they all have ‘legs’.

(BTW, one of the reasons that oddly little-discussed China-made survival game Soulmask is #1 is that it launched a $20 DLC alongside 1.0, and we’re including that revenue. It’s an interesting Conan Exiles-style survival title with some significant quirks that bears more poking-at, and may inspire other games…)

In general, we’re seeing a bit of a groundswell of skepticism on Early Access recently. The issue: a lot of people who want to go into EA do so because their game is ‘truly’ unfinished, which isn’t what most EA buyers want in 2026. And there’s no ‘pot of gold’ upside for 1.0 for most games. At which point, why even chance it? (A quandary.)

Of course, the two above Early Access reasons (‘game’s unfinished’, and ‘we think we can get two marketing beats’) are not the ones swarming the above charts - tho some do get noticed only at 1.0. The best reason to do Early Access is dev-first, and it’s “we can build this title successfully with the community, and they’ll be there with us.”

And when you get that right - as I think Subnautica 2 has, even though they have a soupcon of Reason #1 in the mix - the results can be winning. Just be aware that the surprise and virality of people playing your game for the first time can only happen once. (It’s just a question of when you want to push that!)

Steam’s tag changes: what should you know?

The crew at Valve does not change its game tags very often. In fact, there’s only been eight added to the SteamDB tracker since 2023, and a couple of those are internal to that site! So when Steam put out a bunch of edits yesterday, via a player news post and associated Steamworks dev blog, our ears immediately pricked up.

The tl;dr is that this is more or less a clean-up, “adding 17 new tags, removing 28, and merging/updating a handful of others.” But there’s still a few interesting things here. Here’s our take on the top ones:

The only ‘genre’ to get added was the Vampire Survivors-like ‘Bullet Heaven’: this is ‘focus on upgrades while automatically attacking hordes of enemies’. One Reddit comment notes: “This is great for anyone who was annoyed by survivorslikes clogging up the Bullet Hell tag.” (Unfortunately, they’ll probably receive both tags.)

A lot of popular secondary traits were layered in, too: some of these are genre-adjacent, like Desktop Companion (idlers that use part of your screen) & Wuxia (massive in China historical fantasy). But the bulk of the adds are support tags like Cleaning, Zoo, and Cult (there’s actually lots of cult-themed games out there.)

We love whoever at Valve sneaks in the super specific tags: look, we like capybaras, too but Capybara as a tag seems almost as OCD as adding Birds (which happened in 2023!) But hey, it’s a cute secondary tag and the Capybara Mafia will be delighted.

There’s also some tag removals for a few reasons: duplicative (NSFW & Mature vs. Violent & Sexual Content), subjective (Well-Written, Masterpiece) and specific IP (sorry, Games Workshop, Lego, and Dungeons & Dragons), which are typically “already covered by the developers and publishers setting up franchise pages.”

BTW, this Steamworks post highlights a couple of important 101s on tags: ranking tags is important because “customers can often make assumptions about your game based on the order of your tags”, and “players can also apply tags*” after you put your game live. (*So it’s important to check back on order if you have a popular game, to tweak ‘em.)

It’s a little disappointing not to see ‘friendslop’ get a tag, but we all know that’s mainly because it’s a divisive genre name, implying quality issues. (And sadly, our plaintive pitch for ‘crewlike’ as a name for that genre hasn’t found much interest.) Toodles!

[We’re GameDiscoverCo, an analysis firm based around one simple issue: how do players find, buy and enjoy your PC or console game? We run the newsletter you’re reading, and provide real-time data services for publishers, funds, and other smart game industry folks.]