Revealed: the numbers behind Steam's '24% cut' in 2025

Let's talk history, context, and Thom Yorke. Also: the latest discovery and platform news.

[The GameDiscoverCo game discovery newsletter is written by ‘how people find your game’ expert & company founder Simon Carless, and is a regular look at how people discover and buy video games in the 2020s.]

Hey! With a dash of pepper and soupcon of data exploration, it’s another busy week. Our lead story looks into a number Steam slipped into its 2025 year-in-review that’s been curiously underdiscussed - its actual platform payout by percentage ‘cut’ last year.

Before we start, we dug this Eurogamer piece on the voiceover guy for the PEGI ratings, an ex-ad agency guy who became a go-to VO person for the EU in Brussels (!) He claims: “I reckon the PEGI recordings - PEGI 18 in particular - are the most heard single recordings in history”, due to their trailer inclusions. (The Guinness team is on standby.)

[THE DEEPEST PC/CONSOLE DATA? You can get a free demo of our GameDiscoverCo Pro company-wide ‘Steam deep dive’ & console data by reaching out today - >90 orgs have it. Or, signing up to GDCo Plus gets the rest of this newsletter and Discord access, plus more.]

Game discovery news: Cat Parents gets buzzy…

OK, time to hit those game platform & discovery links pretty hard, starting with the following:

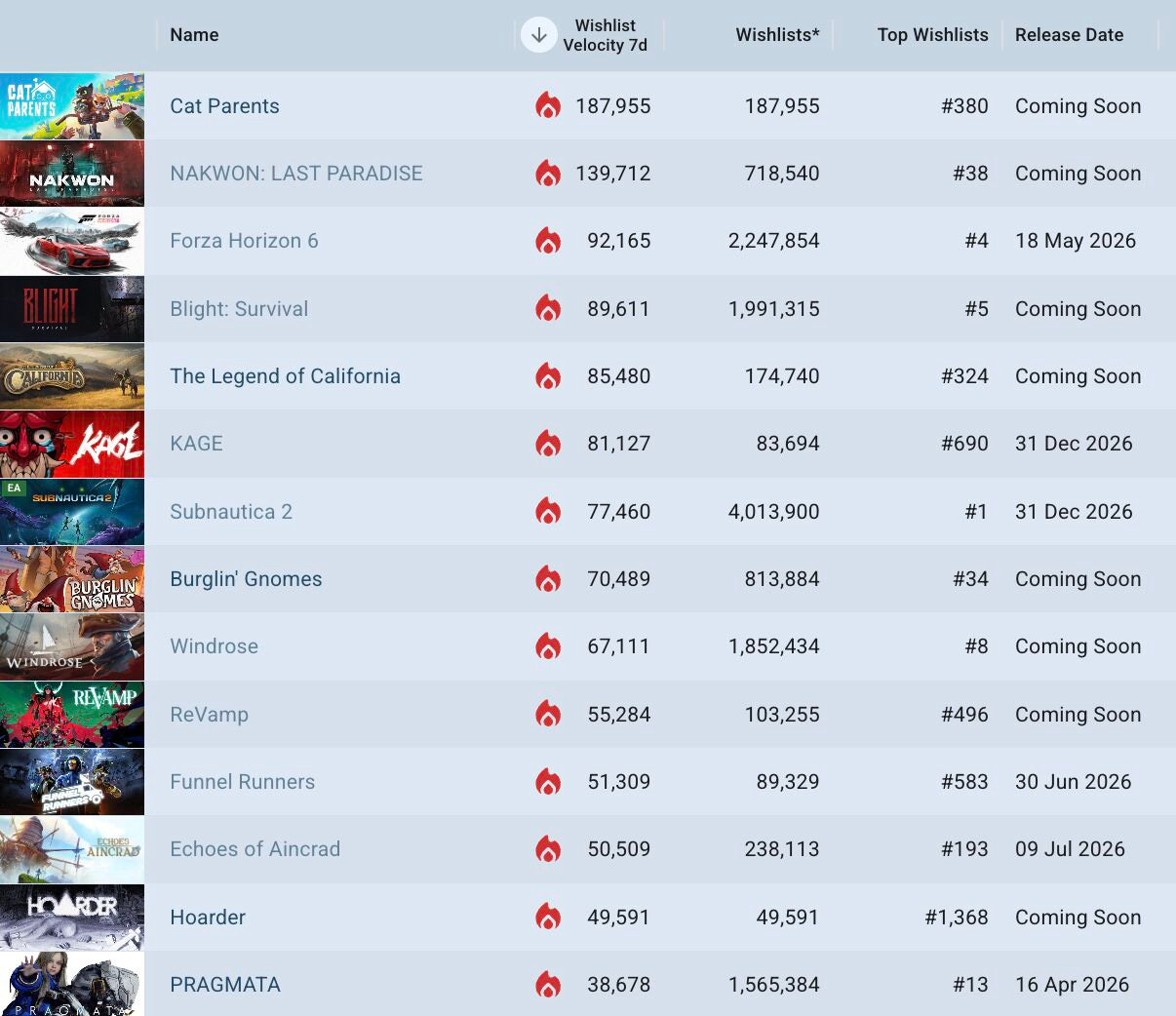

The latest unreleased trending Steam games, according to GameDiscoverCo Pro's 7-day wishlist charts (March 16th-23rd), have Cat Parents straight in at #1. (It’s a first-person cat rescue sim, so… c’mon!) Korean zombie survival game Nakwon: Last Paradise (#2) also had a lot of new interest via a closed Alpha.

Elsewhere, a new trailer for medieval horror action-er Blight: Survival (#4) booster it, and the other new Top 10 entrant is Kage (#6), an anime co-op Megabonk 'fast follow'. Also in the mix at #14? First-person spooky game Hoarder (#14), billed as "a mundane cleaning simulator which spirals into a submerged nightmare."

Fortnite and Epic Games Store owner Epic is laying off >1,000 employees, and Tim Sweeney’s note to employees cites “current consoles selling less than last generation’s; and games competing for time against other increasingly-engaging forms of entertainment” as key reasons. (Multiple Fortnite add-on modes are also ending.)

We’re seeing new delistings of PlayStation ‘shovelware’-y publishers, with ‘easy Platinum Trophy’ kings Nostra Games saying “We’re unable to provide an exact reason because it wasn’t shared with us.” (CGI Labs, less Trophy-farm-y, but very clone-y and keyword squat-y, e.g. Bodycam Stray Kitty, also got its games pulled.)

Slay The Spire’s 2 recent ‘review bomb’ for early card nerfing is a prime example of why Steam changed its review positivity % to be language-specific (the vast majority is from China!) Indeed, as PC Gamer notes, no access to Discord or Steam forums means that Chinese players often end up venting direct in reviews…

As my colleague Alejandro noted on Sunday: “Spring just arrived, and with it a new CCU peak for the Steam platform.” Concurrents went up from 42.04m (Jan. 2026 high) to 42.32m CCU for ‘logged in to Steam’, and from 13.4m (Jan.) to 13.82m actually playing a game.

Bloomberg is citing sources as indicating that Nintendo “plans to make 4 million units of [Switch 2] this quarter, a third less than the 6 million it had originally planned to produce.” It should still hit 20m sold this fiscal year, but there’s still behind-goal U.S. sales, despite good sellthrough of a cheaper, loss-leading Japan-only version.

The latest Circana U.S. game hardware/select software charts of Feb. 2026 show spending up 1% to $4.6b, helped by Resident Evil: Requiem. Hardware rev was up 22% year on year (with Switch 2 up YoY, but PS5/Xbox down), and Requiem’s launch week dollar sales outpaced Resident Evil: Village by 60%. (Good launch!)

Some notable changes upcoming in how brands (& dev studios dealing with brands!) work on Roblox: “Starting next year, Roblox will begin charging creators a fee to publish brand integrations inside their virtual experiences, with payments scaling based on the experiences’ user traffic and engagement.”

We’re been getting/sending reports about a) slow ‘wishlist email’ sending for the Steam Spring Sale or b) slow Steam back-end reporting of sends. (It could be either, and emails are still quite important to sales.) You can see email delivery rates and conversions at the very bottom of your game’s wishlist actions page.

ICYMI (since we did), Meta’s Chris Pruett has a pretty transparent blog post about Meta Quest’s 2025 results & plans. Notably: >100 VR games generated >$1m in gross revenue on the Meta Horizon Store, which ain’t bad. And overall revenue is still premium-first, “but IAP grew significantly in 2025, by over 10%.”

How Steam’s ‘24% cut’ in 2025 breaks down….

As trailed above, it was interesting to see a particular tidbit buried in Valve’s giant, multi-thousands of words year in review back on March 6th, and we wanted to hold it back and analyze it. Look, we’ll bold the interesting bit(s):

“Since the 2018 announcement of the 75% and 80% revenue share tiers, more and more games from developers big and small have reached new higher revenue share. The revenue share paid out across all non-Valve games on Steam in 2025 was 76%, and that does not include any revenue developers may earn selling free Steam keys outside of Steam.”

Valve has done very little public pushback on the ‘Valve stop taking a 30% cut, you’re horrid’ lobby - who are increasing, as mobile platforms make concessions and the biz is squeezed. And this - revealing that the ‘real’ Valve payout is 24%, is a notable one.

But how is that 24% broken down? GameDiscoverCo estimates the daily revenue of every single game on Steam, so we thought we’d try to break down all Steam revenue in 2025 by tier paid out. Yes, really. And here’s the estimates we got to:

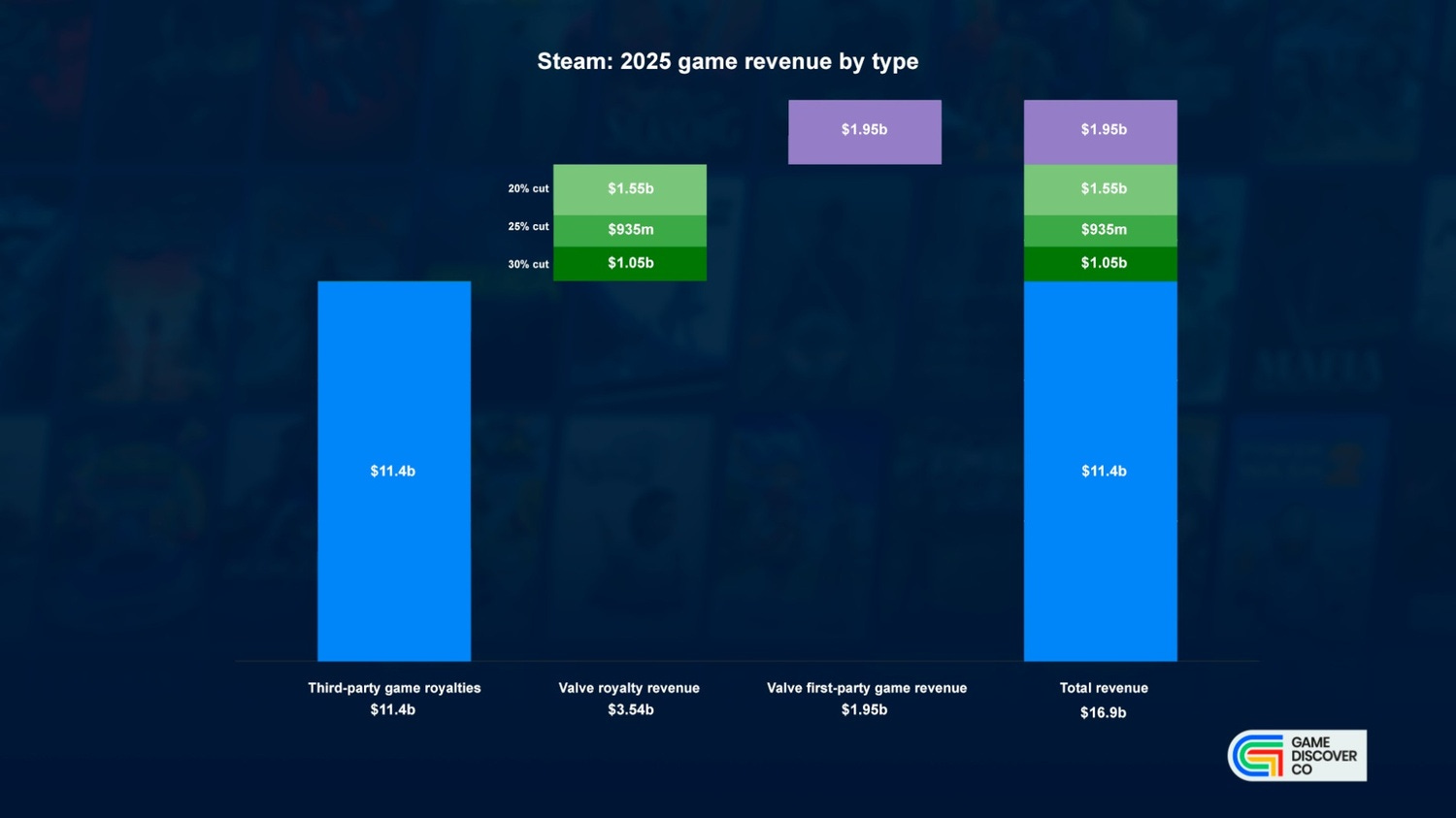

$16.9 billion: total gross revenue on the Steam platform in 2025.

$1.95 billion: gross revenue for Steam’s own games*, mainly Counter-Strike 2. (*It’s difficult to work this one out, cos CS2 is #1 so often. Either way, it’s a big #…)

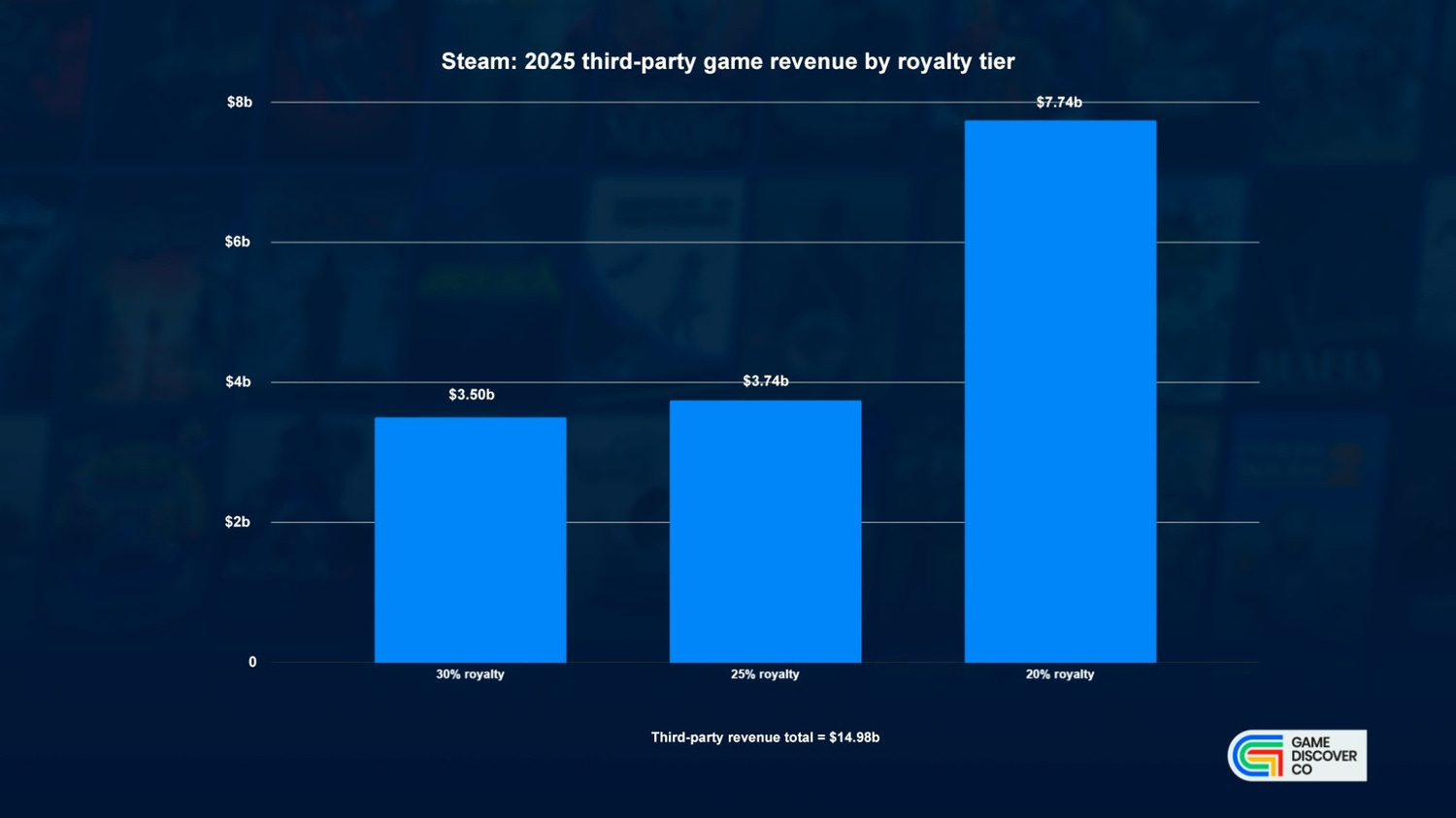

$14.98 billion: gross revenue for all third-party Steam games in 2025.

So, remember, now we need to break this down by royalty tiers, given “when a game makes over $10 million on Steam, the revenue share for that application will adjust to 75%/25% on earnings beyond $10M. At $50 million, the revenue share will adjust to 80%/20% on earnings beyond $50M.” And here’s what we came up with:

We weren’t really sure what the shape of this graph would look like. But some immediate takeaways from it:

The ‘30% royalty tier’ is actually the smallest of the three: ‘only’ $3.5b of the $14.98b that Steam got royalties on in 2025 (that’s 23%) is paid with 30% going to Steam. (Of course, that rate is what the vast majority of individual devs get.)

The kings in the ‘20% royalty’ category made 52% of all Steam revenue: those whose game grossed $50m LTD (after refunds, etc) made up $7.74b (52%) of every dollar spent on Steam in 2025. (The ‘25% cut’ rate was, ironically, 25% of the total.)

So we can now see what Valve gets from each of these tiers, and we get to this:

According to our estimates, Steam is grossing about $1.05 billion from the ‘30% royalty’ tier, $935m from the 25% tier, and $1.55b from the 20% tier, for a total of $3.54 billion Steam platform royalty in 2025. And this is, it turns out, 24% of that total non-first party game revenue of $14.98b. (So we’re hopefully ballpark, here.)

Finally, let’s check out all of this 2025 Steam revenue by type in a nice stacked graph, for context:

So that’s the math(s). Now let’s talk about the vibes. It looks like Valve ‘gave up’ $770 million in ‘20% tier revenue’ and another $190 million in ‘25% tier revenue’ in 2025 - so almost $1 billion - vs. just sticking with 30% rates. That’s extremely non-trivial.

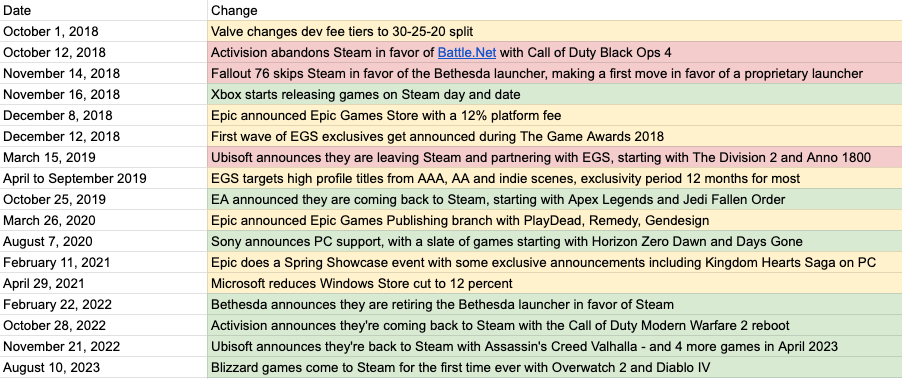

A reminder on why they did it, from the Nov. 2018 announce: “The value of a large network like Steam has many benefits that are contributed to and shared by all the participants… Successful games and their large audiences have a material impact on those network effects so making sure Steam recognizes and continues to be an attractive platform for those games is an important goal for all participants in the network.”

This was such a typically wonk-y reason for Valve to change its rates. And I think it made a ton of sense in 2018, when there was a proliferation of platform competition, and big publishers with changing platform strategies. I got my colleague Alejandro to compile a rough timeline of what happened, and it’s so good I’m just cut-pasting it:

Anyhow, in the more than 7 years (ugh, really!) since that shift, it’s safe to say that big publishers’ own platforms on PC haven’t done well. Steam is, more and more, the ‘main thing’ for PC games. Is it because the biggest games get better high-end royalties? We can’t tell. But that’s why Steam did it, and network effects are real.

So what’s next for those in the 30% tier who, say, want a lower royalty? You can’t really ‘make Steam do a 24% royalty for all games’ - putting the toothpaste back in the tube from the 2018 change - because there’d need to be public companies (big and small) at 20% perma-adjusting their profits, alarming shareholders, etc.

As for suing Valve - sure, some companies will yield to legal/antitrust threats, and we hear there’s still some of those suits ongoing. And I was reminded by this article on Google Play’s recent rate cuts that this had already helped small devs: “The actual win for the [small mobile dev] long tail happened in 2020/2021, when both Google and Apple, spooked by the [Epic] lawsuits, cut rates to 15% for the first $1M in annual earnings.”

However, we’ve got news for you - which probably isn’t news. ‘Changing the revenue tiers for the small guy, for PR reasons’ is the last thing Steam will ever do, because they’re famously not like that. (And to be fair, Steam revenue is much less top-heavy than mobile.) They need a logical, self-contained reason to do it.

What I will say is that, if our numbers are right, it’s ‘only’ $130 million per year - just 2.4% of Valve’s 2025 non-hardware Steam-centric revenue - to go to a 25% royalty as a maximum and eliminate the 30% tier entirely. And isn’t that worth it, just to stop me writing editorials about it constantly? Toodles…

[We’re GameDiscoverCo, an analysis firm based around one simple issue: how do players find, buy and enjoy your PC or console game? We run the newsletter you’re reading, and provide real-time data services for publishers, funds, and other smart game industry folks.]

Lovely breakdown and analysis!

Your numbers seem spot on, excellent job