2024: what the ****'s going on? (In PC games?)

A general market musing, plus Team17 financials and lots of news.

[The GameDiscoverCo game discovery newsletter is written by ‘how people find your game’ expert & company founder Simon Carless, and is a regular look at how people discover and buy video games in the 2020s.]

Welcome back, folks, and it’s another week on the ‘let’s explore who’s buying video games using words and pictures’ train. So choo-choo, let’s try not to get bricked up in a tunnel, and keep chugging along happily to our (high sales number?) destination…

Also: we really wanted to make today’s newsletter entirely about the GameScent, which “uses the magic of AI to inject scents into the air, based on what's happening from moment to moment in your game.” (Anybody remember when Philips amBX used a game-triggered fan?) But our publisher* (*me) over-ruled us. Instead, here’s this….

[HEY YOU: you can support GameDiscoverCo by subscribing to GDCo Plus now. You get full access to our Steam data back-end for unreleased & released games & weekly PC/console sales research, Discord access, eight detailed game discovery eBooks - & lots more.]

2024: what the ****'s going on? (in PC games?)

We talk PC and console game trends a lot, sure. But we were prompted by this LinkedIn post - screenshotting a comment from The Long Dark’s Raphael van Lierop - to pause and go a bit deeper. Here’s Raphael’s quote, about Manor Lords’ success:

“Most of the big hits on Steam this year (apart from Helldivers) have been from small, independent developers in genres that were either abandoned by triple-A publishers (ex. city builders, RTS, etc.) or ones that have never been fully mastered by triple-A publishers (ex. survival).

It's also no coincidence that many of the biggest successes have been "surprises". It speaks to the potential for something to go viral on a platform like Steam, which is as much a social platform as it is a storefront (very different from other digital stores, where there is almost no community component)….

…It largely comes down to (a) general fatigue with the triple-A approach and the lack of perceived "value" at that price point, (b) the network effects of something like Steam, which is much more than just a digital store, and (c) genuine interest in innovation and genres that have been largely abandoned by mainstream game publishers.”

When we discussed this in GameDiscoverCo Plus’ member-only Discord, a couple of key comments surfaced. Firstly - while people broadly agreed with Raphael, esp. on PC genres - they did note that standout indies are often ‘good news in a sea of bad news’, and mask a generalized lack of success vs. dev expectations across the board.

As I said in Discord at the time: “It's easy to be an indie, but the empirical chances of succeeding massively kinda suck. Which, yeah, is slightly different framing to 'small, indie developers are breaking out', if you squint.” Still, bigger games just have a tougher time making their budgets back, so look even worse in comparison…

Secondly, some of the ‘surprise’ over certain games’ success is more due to filter bubbles on information, than anything else. (It’s big - it’s just not big in the bits of the Internet that you actually use?)

GameDiscoverCo estimates that Manor Lords - which we’ll be profiling shortly - was perhaps the ‘most wishlisted’ Steam game to debut since the start of 2023, with the exception of Bethesda’s Starfield. We have it outperforming its Week 1 expectations by 80% - that’s a lot, but not 580%!

Hit PC games: geography & resources don’t matter

However, there are also plenty of indie titles that come out of ‘nowhere’ - or at least ‘a smaller filter bubble’, haha - and outperform. This is generally due to influencer, Steam and word-of-mouth virality.

A great example: last Friday’s GameDiscoverCo Plus newsletter looked at the mixed reactions to high-budget sci-fi RTS sequel Homeworld 3, which has already dipped to a 24-hour high CCU of ~2,500 on Steam.

Conversely, solo dev co-op roguelite Rabbit and Steel launched a few days earlier, and maxed out lower than Homeworld, but hit ~4,300 max 24 hour high CCU today - stronger ‘long tail’ results. (For reasons we’ll be discussing in the newsletter shortly!)

That indie title is only $15 instead of Homeworld’s $60, sure. But Odyssey Interactive’s Ryan Rigney has a comment on what’s happening, in abstract: “There is an epochal shift happening in the games industry, and many in AAA don’t understand it. The advantages that big studios and pubs once had are eroding to nothing. While AAA games fail to recoup costs, indies are - almost daily - shipping games that sell 100k or more units.”

But what are the concrete trends driving this? We’ll try to list three, and then step away to let everybody breathe for a second:

You can make amazing-quality games from anywhere in the world: there’s just no (financial) reason for game devs to be in high-GDP countries. Thanks to democratization of engines & assets & the Cambrian explosion of PC games, you can be in Serbia, Thailand, and beyond - where cost of living is very different.

You aren’t necessarily working full-time on your game: we’ve talked about the deprofessionalization of games in the past. But again, in the spirit of ‘On the Internet, nobody knows you’re a dog’, you might be a student, you might have a dayjob, and these things a) increase the # of games b) allow niches to flourish.

You can make games that look like a 20-person dev team with 1 core dev: there’s plenty of games to cite here - and Manor Lords recently got some weird static over this. But the truth is simple - titles like Manor Lords & Animal Crossing-y hit Dinkum (above) were primarily created by one person. And… we just can’t tell?

The point here is - yes, video games are a profession. And there’s still plenty of money in the space. But we’re starting to reach the point where games are just not a stable long-term career for some subprofessions in high-GDP countries.

And the reason you’re seeing so many layoffs, and the largest companies making less, bigger video games, as Game File noted - is that the economics of making and distributing games have massively changed over the last decade. (Firms’ decisions to lay off while being profitable elsewhere sucks, but is also… capitalism at work.)

Finally, as we repeated earlier, this doesn’t mean the ‘grass is greener’ for indies. Just to repeat: there are less winners as a % of entrants. But many of them are winning with new games on a much lower success scale - being lower-cost and bootstrapped.

And we’ll carry on highlighting those who win - and some that don’t. That way, we can understand how successes are discovered and consumed in today’s PC/console biz.

Team17: key lessons from the firm’s 2023 results…

With more companies - and less time for biz journalists to analyze - comes a lack of detailed coverage on some firms! As an example, we saw almost nobody delve into Team17’s recent 2023 annual results [.PDF link], a pretty large omission. So we’ll have a quick, amateurish hack at it.

Overall, Team17 is sporting a post-COVID hangover similar to many PC/console game firms. Revenue was up 12% to £160 million ($203m), but gross profit down 17% and adjusted EBITDA down 39% to £30 million ($38m). Here’s what we saw in detail:

Team17 is going back to more modest third-party game funding: they revealed that “the majority of third-party game investments are expected… to fall in or below the range £1.0 million to £1.5 million”, while noting: “we had seen an increase in the budgets of games… the focus of new [funding] will in future be firmly in the Indie space.” Clearly some poor ROI on bigger-budget titles here.

Once again, sales of older titles are providing much strength: they note “the Group's back catalogue continues to strengthen, growing at 10% with revenues of £113.6 million (FY 2022: £103.5 million) representing 71% (FY 2022: 73%) of total revenues.” Actually, games like big 2023 hit Dredge meant this back catalog % wasn’t as high as many competitors.

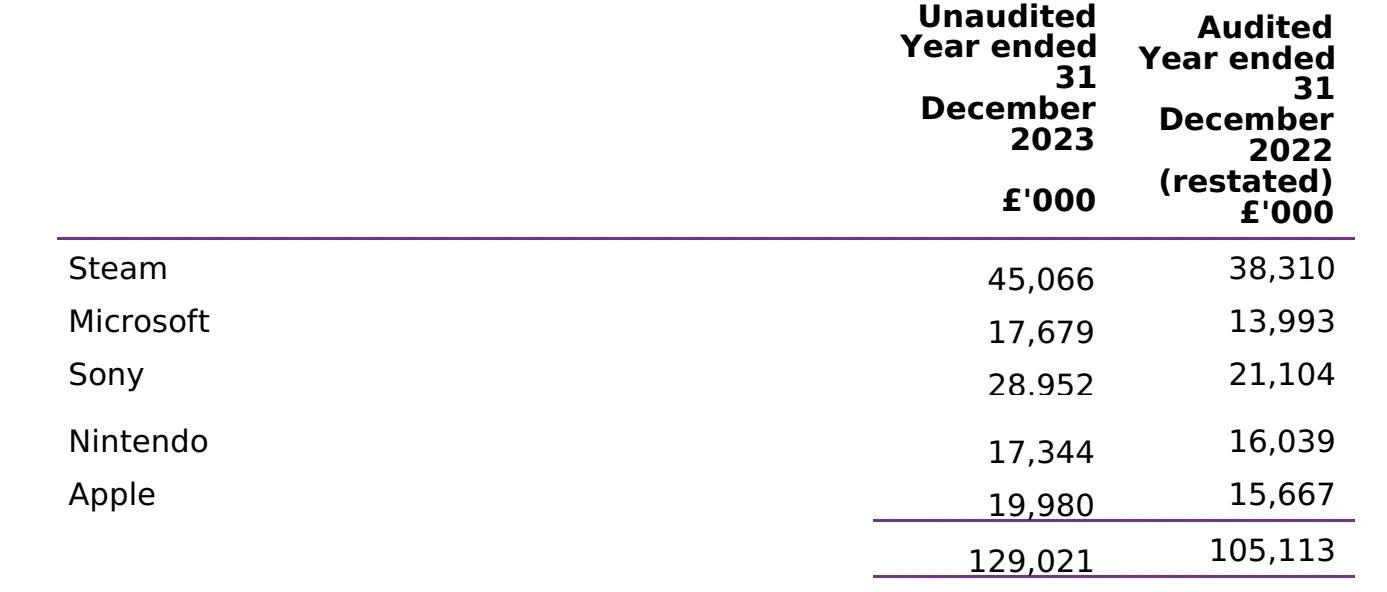

Diversification beyond PC/console has been mixed: you may be wondering why Team17’s key revenue sources (above) include so much Apple. That’s due to kids game service StoryToys, bought in 2021 - >320k subscribers! But sounds like buying What The Golf? publisher The Label to get games into Apple Arcade-like services has been a disaster, with most of its value written down.

We did think that Team17’s revenue as a whole - listed for any vendor with >10% of total yearly revenue* - was interesting. Of that slice, it’s 35% PC, 22% PlayStation, 15% Apple/iOS, 14% Nintendo, and 14% Xbox. (*Don’t forget that the company owns PC sim specialists Astragon also, and Game Pass/PS+ deals may be included in the $, too.)

It’s not been a pleasant ride inside Team17, with “headcount reduced to 348 as of 31 December 2023 (as at 31 December 2022: 392), reflecting the impact of the Games Label restructuring review and increased utilisation of an outsourced studio resourcing model.”

But from a pure financial planning point of view, decent amounts of back catalog and a more diversified portfolio may help to stabilize things. Fresh Dredge-sized hits are still needed to avoid poor year-on-year comparisons, though…

The game platform & discovery news round-up..

To round things out, let’s take a look at the game discovery & platform news we’ve painstakingly assembled since last time out. It looks a bit like this:

Reports say that Microsoft has decided to include Call Of Duty in its Game Pass subscriptions - the implication all along, though some wondered if it would happen - with more details in the June 9th Xbox showcase. The Verge adds that the company “has been considering raising the Xbox Game Pass Ultimate pricing again.”

UploadVR goes through the reasons that Meta’s Quest 3 ‘Lite’ may be incoming - Quest 2 price cuts and ‘out of stock’ warnings for certain models, a Meta roadmap leak last year, “Quest firmware dataminer Samulia discover[ing] a new headset codenamed Panther”, and a good many other indirect sources besides.

Two super-interesting console stats? First, Stephen Totilo spotted that, per Sony, only ~50% of their 118 million monthly active PSN accounts are on PS5 - lots of active PS4s, still! And second, Niko Partners’ Daniel Ahmad estimates that PS5 shipped almost 5x the Xbox’s hardware totals last quarter. (4.5m vs. a million?)

The ESA’s 2024 ‘Essential Facts About The Video Game Industry’ report is out, showing “61% of Americans ages 5-90 play video games, meaning approximately 190.6 million people play games at least one hour each week in the United States. The average player is 36 years old, and the average adult player has been playing for 17 years.”

The Epic/Apple lawsuit is still rumbling through its aftermath, and “Judge Yvonne Gonzalez-Rogers remains unconvinced of Apple's rationale for claiming it is complying with her original [allow alternate payments on the App Store] order, following testimony from Apple Fellow Phil Schiller.” An Apple-hired research company said 12.7% was the lowest ‘acceptable royalty rate’, so the judge is asking - why set it to 27%?

Here’s a small and helpful new Steam UI widget I spotted: “Starting a few days back, the web version of Steam's front page (https://store.steampowered.com) sometimes more actively prompts people to sign in to Steam desktop.” Good for attribution & more logged-in players, right?

Here is a preview of Twitch's mobile app overhaul, out this year. Zach Bussey says: “It's effectively TikTok's app design but swaps the Browse/Friends position. Path of least resistance, I suppose?” (Via Zach’s excellent ‘Today Off Stream’ newsletter.)

The Verge has a look at Sony’s new PlayStation PC overlay (above) - aka ‘the PlayStation Network integration’ for PC. Overall:“There are five main sections: search, friends, Trophies, profile, and settings” - with friends & trophies the most relevant.

Following up the Another Crab’s Treasure newsletter from last week, community lead Paige Wilson had an illuminating Twitter/X thread explaining that “our marketing efforts could not have been done without the help from EVERY. SINGLE. MEMBER. OF. OUR. TEAM” - showcasing the custom assets used for viral posts.

The Netherlands’ ‘authority for consumer & markets’ has fined Epic 1.125m Euros “for using unfair commercial practices aimed at children in its Fortnite game”, specifically ‘dark patterns’, “using ads which directly exhort children to make purchases, and by using misleading countdown timers for items on offer.”

Esoteric microlinks: an industry worker explains why the U.S. animation industry ‘is collapsing’; here’s four minutes and thirty-eight seconds on ‘marketing attribution’ you shouldn’t miss; the changing back-list & self-publishing trends in the book industry make interesting comparison to games.

Finally, roused by a new RockPaperShotgun article about UGC in super-goofy music game Trombone Champ, we discovered modder Gloomhonk’s tracks. (You might know them modding UK Prime Minister Liz Truss’ resignation speech into the game.)

But their other ‘big hit’ is this amazing trombone cover of Journey’s ‘Don’t Stop Believin’’, where the guitarist is repeatedly trolled by the trombone player taking over his solos. (Watch for the reaction at the 3-minute mark, and the very end of the song…)

[We’re GameDiscoverCo, an agency based around one simple issue: how do players find, buy and enjoy your PC or console game? We run the newsletter you’re reading, and provide consulting services for publishers, funds, and other smart game industry folks.]

💚🔥🌟

Thanks for bringing up that indie games are not necessarily the counterpoint to AAA woes (a topic you've covered and illustrated well in the past).

I'm seeing a lot of gaming commentators, especially on YouTube, try to build a narrative about the indie market as the shining light to gaming industry woes. But none of them point out, as you have in the past, that the majority of indie games fail because it's a very crowded and demanding market right now. I look at a lot of demos - the quality out there is astounding. But getting people to notice your game is so hard. These days, if you can manage getting 300 reviews on Steam, that's a big deal!

There is this narrative that indie is the new saviour of gaming. But I think it's primarily encouraged by people who don't have a lot of exposure to the absolutely saturated market - and that's just Steam. Let's not talk about getting noticed on something like Itch!